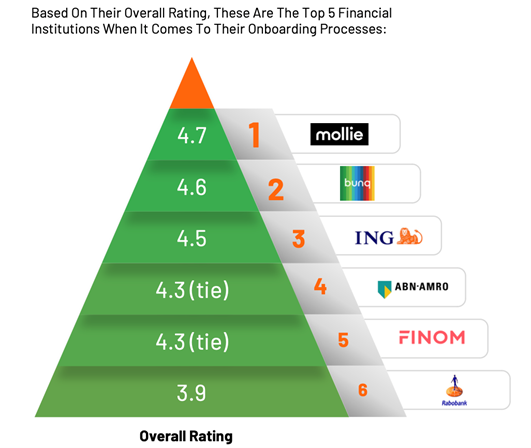

How is this art performed in practice? Last year we conducted a comprehensive benchmark study on the quality of the onboarding processes at 13 financial institutions active in the Netherlands: ABN AMRO, Bunq, CCV, Finom, ING, Knab, Pay.nl, Multisafepay, Mollie, Triodos, SNS Bank, Stripe and Rabobank.

The main objective was to find out how well these processes are designed and executed from the perspective of small and medium-sized (SME) companies looking to become customers. For this purpose, we established a web shop to run the onboarding processes and assess and compare them, based on the following set of evaluation criteria:

- User experience: the ease with which the page to become a customer can be found, the reachability and availability of communication methods, the conciseness of texts and the (number of) available languages.

- Speed: the time it takes to get a response, the number of interactions, the relevance of the questions and the duration of the entire process.

- Customer due diligence: the way compliance with legal KYC obligations is organised, i.e. automated or manual, the extent to which clear language is used both during the process and in the contract, and the options for signing the contract: digitally or only physically or both.

- Product offering: this criterion includes clarity about the types of products and services, incentives and the accessibility and transparency of the price schedule.

All operational onboarding processes were scored on these four criteria on a five point scale, ranging from poor, fair, good, very good to excellent.