SPAA is coming

In an earlier article on open banking we briefly discussed SPAA, which stands for SEPA Account Access. SPAA, an initiative of the European Payment Council (EPC), is a new, voluntary payment scheme. Enrollment for banks and third-party providers has opened on 1 September 2023.

The scheme’s ambition is to drive ‘open payments’ in Europe and to become the de facto European standard in the field of open banking. SPAA is not a payment means or a payment instrument itself, but it offers a way to transport information in relation to payment accounts and transactions via APIs. It is envisaged that the scheme will evolve further over time to support more elaborate functionalities, in line with market demand, possibly even beyond payments.

It works through Payment Initiation Services (PIS) over the SCT Inst rails. All currencies in the SEPA zone are supported, so in addition to the euro, for example, also British pounds and Danish crowns.

SPAA focuses on Asset Holders and Asset Brokers

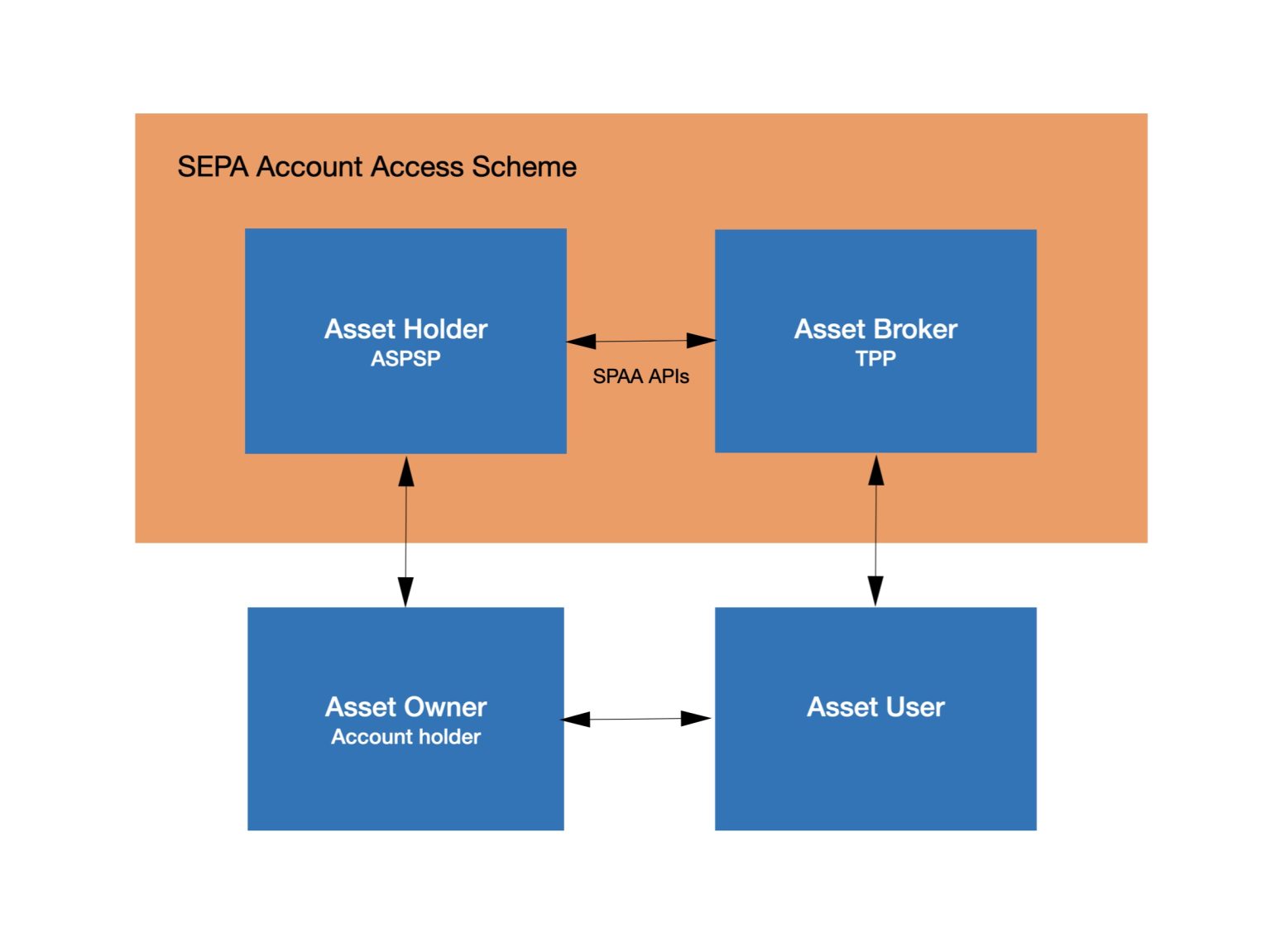

SPAA focuses in particular on the relationship between so-called Asset Holders (the party that manages the data on behalf of a private individual or organisation) and Asset Brokers (the party that requests access to the data in order to provide a service to that same private individual or organisation). (1)

A typical Asset Holder is a bank, or the ASPSP in PSD2 terms. A typical Asset Broker is a fintech company that does not offer (current) accounts itself. In the remainder of this article we use AH Bank (Asset Holder) and ABFinance (Asset Broker) as imaginary examples. The two roles are part of a generic 4-corner model that is reminiscent of the model used in the cards ecosystem to distinguish between issuing and acquiring roles.

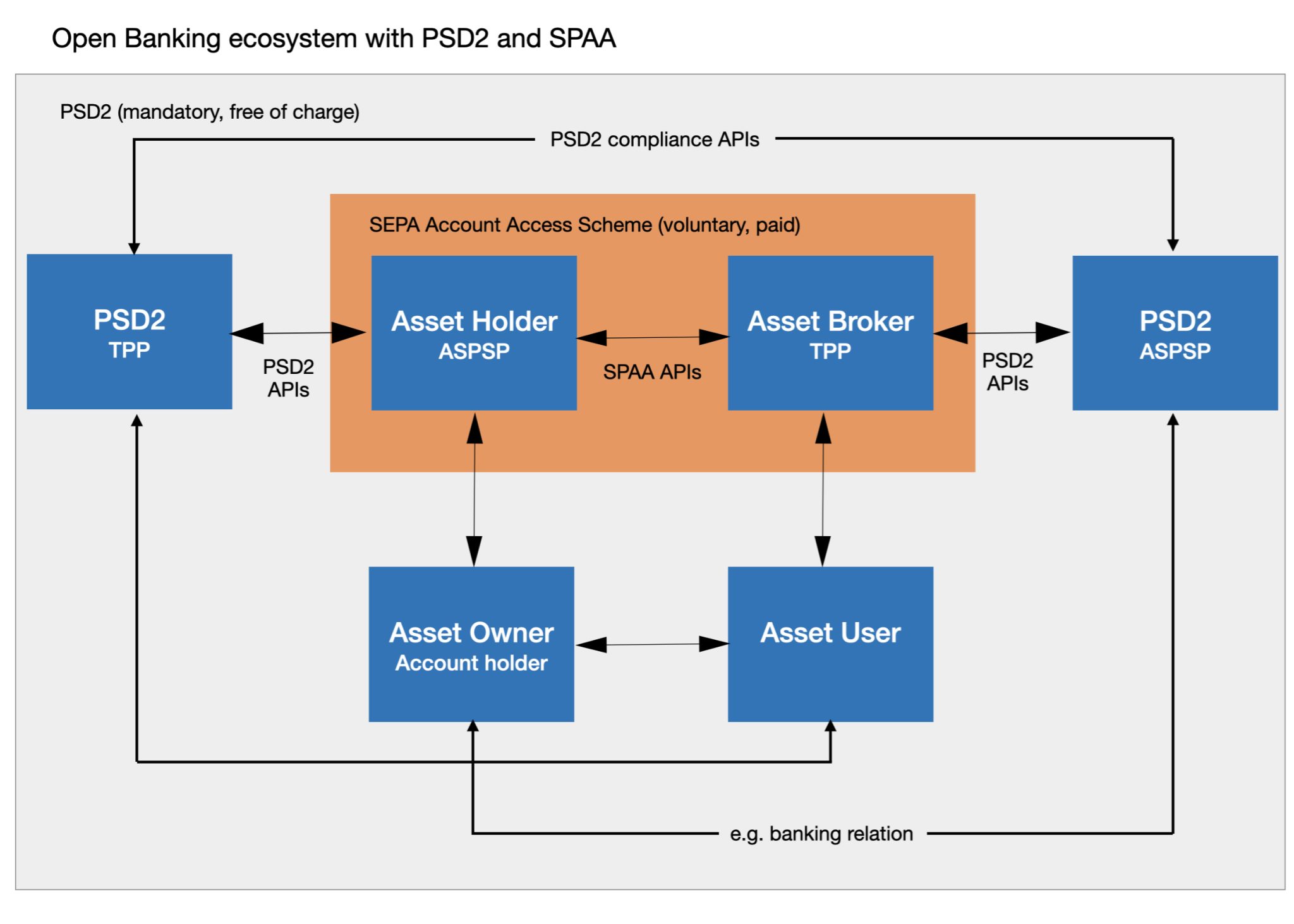

PSD2 vs SPAA: risk of a fragmented ecosystem

Our Asset Broker ABFinance will soon be able to choose. Does it extract the desired payment data from the freely available but limited and troublesome PSD2 APIs? Or does it opt for the “industrial-quality” APIs via SPAA, with a better customer journey, in exchange for what the SPAA MSG calls a “small fee”? And what if not all banks relevant to ABFinance’s market participate in SPAA? So that ABFinance has to continue to support the PSD2 APIs in addition to the SPAA APIs?

Something similar will soon apply to AH Bank: it remains obliged to offer the PSD2 compliance APIs, but as a SPAA Asset Holder, it will also offer a similar basic service that functions better in practice.

Notes

1. SPAA focuses mainly on the relationship between so-called Asset Holders and Asset Brokers. The definitions of these roles are similar but more generic than the ASPSP and TPP roles in PSD2 respectively. The aim is that they can be used more broadly than just for payment data, with a view on future access to financial data.

With payment data as an example: a bank that makes payment data available is an ASPSP (PSD2) or an Asset Holder (SPAA). A company that wants to use that payment data is a TPP (PSD2) or an Asset Broker (SPAA). The owner of the data, the Asset Owner, a private individual or organization, has a business relationship with the Asset Holder. A so-called Asset User can, for example, be a merchant who uses the data requested by an Asset Broker. All this subject to permission from the Asset Owner.

2. Both documents are included in Annex I of version 1.1 of the rule book.