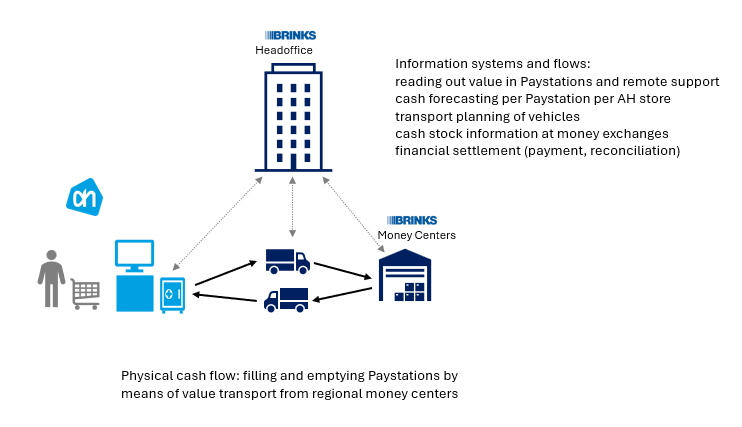

You may have come across one by chance, at a shop where you do your daily shopping for example; the so-called Paystation, a closed cash register system that automates manual cash handling at the checkout.

Cash remains an important means of payment and many consumers still pay for daily shopping with banknotes or coins. In addition, cash is crucial for the inclusion of socially vulnerable citizens, such as the elderly or lower-income groups.

Given market developments in retail (staff shortages, increased use of self-checkout, disappearance of service counters, ban on tobacco sales), there is a need for automating processes and increasing security. This can be done by automating cash processes. For example, when this solution was implemented at Albert Heijn, we saw an increase in the use of the self-checkout.

We ask Martijn Wiersma, Marketing & Sales Director at Brinks, about this successful cash solution innovation in the retail market.

How successful has this strategic shift been?

As it is with innovations, it takes time for new propositions to prove themselves and become the standard. We are no doubt all familiar with the so-called hockey stick effect where it takes a while for the market to show exponential growth. Fortunately, the willingness to invest has only grown in the declining cash market. Retailers are eager to move towards automation of their business processes, which is why we as an organisation have experienced the highest growth in the past period.

We also see the Netherlands, in particular, as a guiding country for these innovations. Dutch consumers are quick to accept new innovations. Furthermore, the Netherlands has a relatively high average labour wage, making it easy for retailers to make a business case.