As consultants operating in the payments space—whether working with banks, merchants, or PSPs—we often focus on infrastructure, products, and implementation. Understanding user experience is crucial in our projects: how the product behaves, how users move through it, and friction points.

Here, an excellent example of how a seamless payment flow works is Wero.

That’s why, below, we’ll share a step-by-step walk-through of a transaction we executed with it. We were positively surprised by the peer-to-peer payment experience.

What is Wero?

Wero is the digital wallet and mobile payment solution backed by the European Payments Initiative (EPI) and a group of European banks and acquirers.

Key facts:

- Launch: Initially live in Germany, France, and Belgium in 2024

- Current core use-case: P2P payments using a phone number or email, not needing an IBAN each time

- Roadmap: Expansion into e-commerce, point of sale (POS), subscriptions, and value-added services over 2025-2027

- Motivation: European payments sovereignty—reducing dependence on U.S. card and wallet schemes

In other words, Wero is positioning itself as the next-generation European P2P wallet, embedded into bank apps with ambitions to go beyond basic transfers.

Our Transfer Experience: Step-by-Step

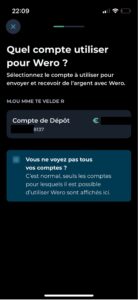

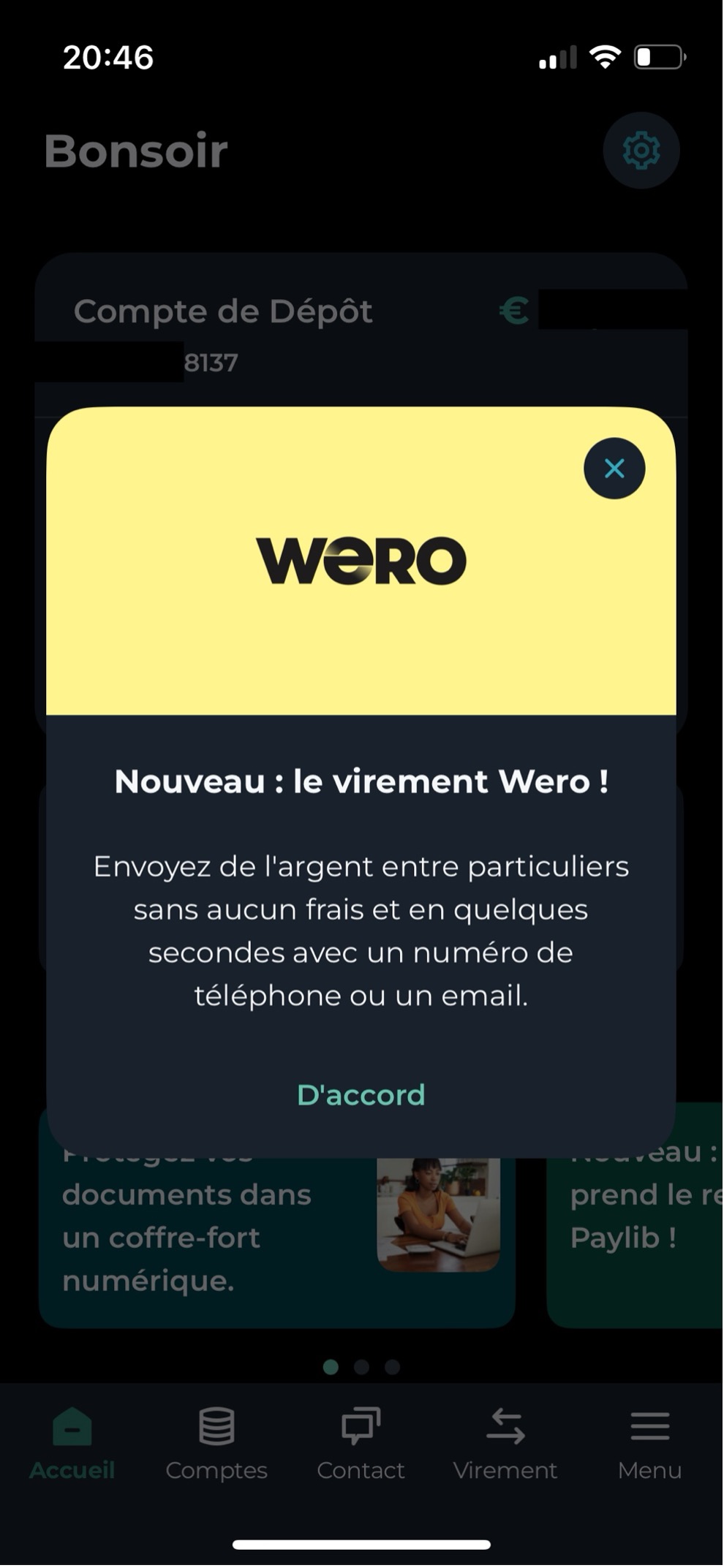

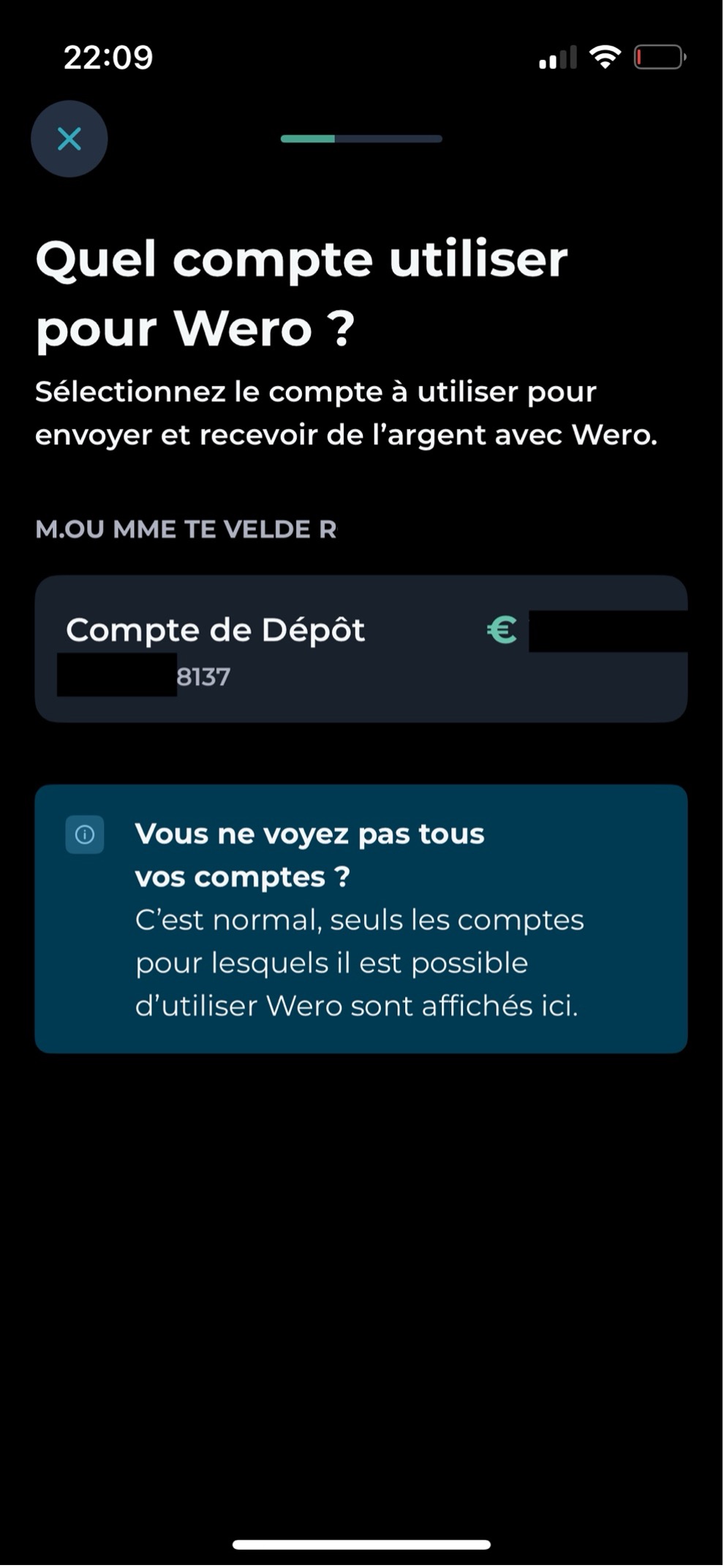

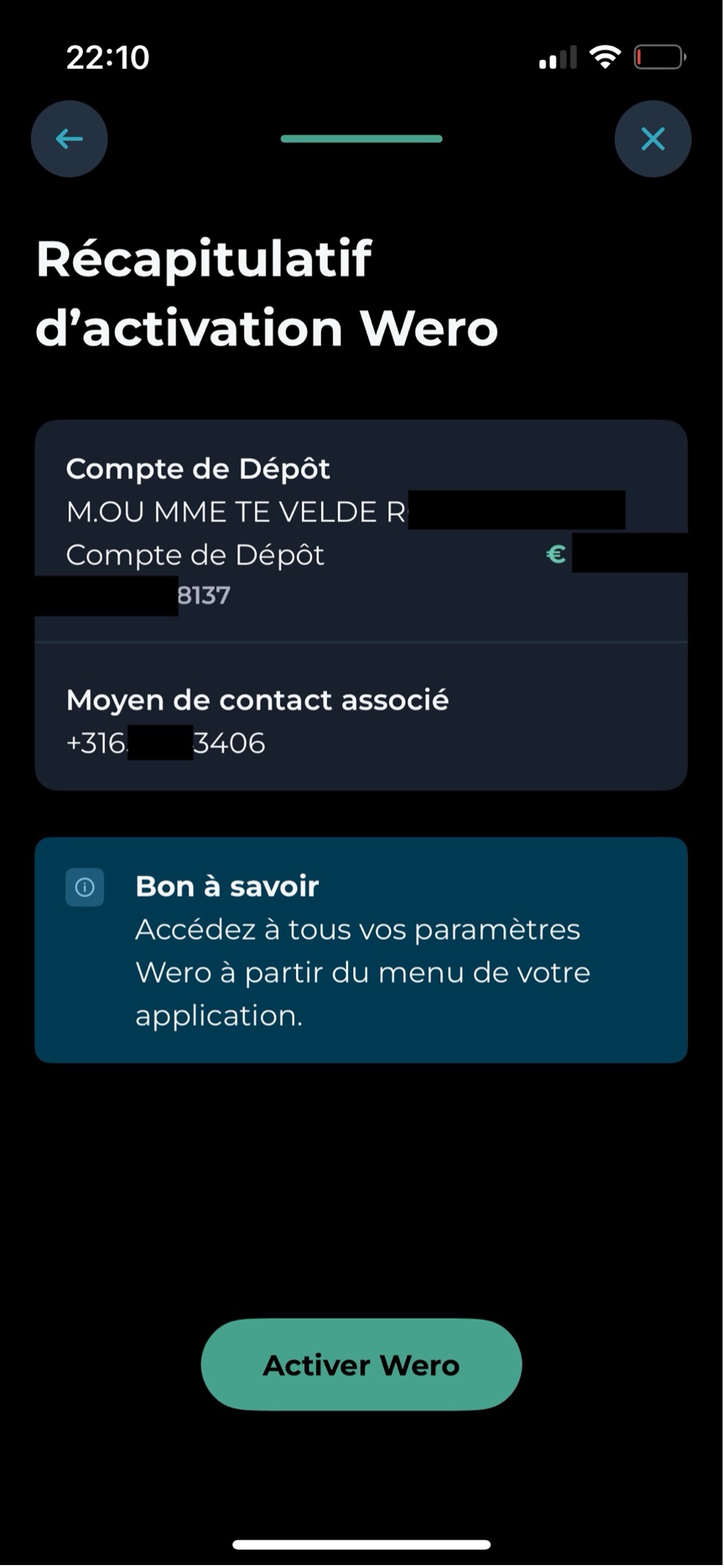

- Setting Up Wero for First Use

We opened our Credit Agricole app in France where Wero is supported. The bank was clearly promoting Wero with a welcome message: “New, the Wero transfer!”

In France, Wero was introduced in 2024, replacing Paylib, which had 15 million active users per month and €6 billion in volume during 2023-2024.

Setup was super easy: Choose which account you want to use, select your identifier (we used our mobile number), link it to your IBAN, and confirm. That’s it.

- Initiating the Transaction

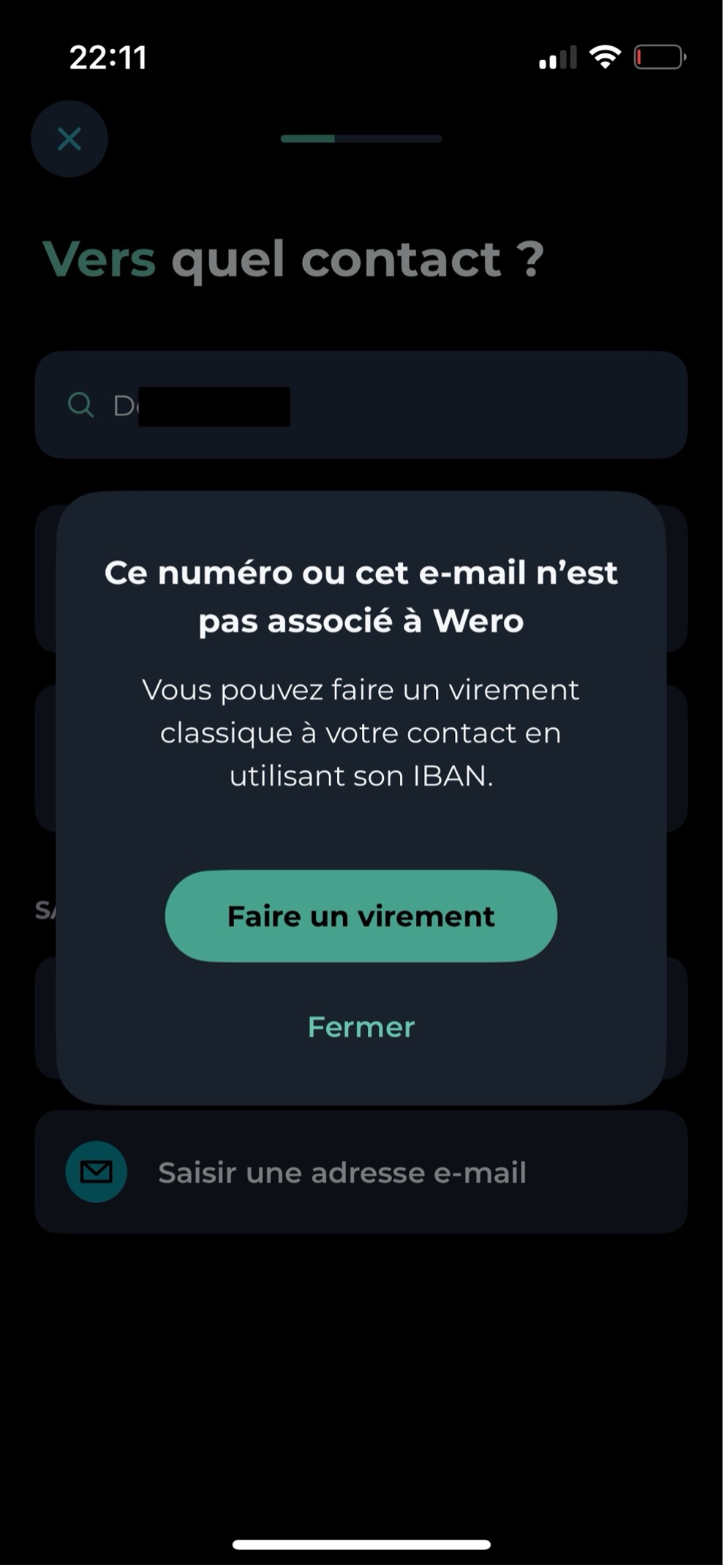

After confirming we wanted to initiate a transaction, we selected a contact from our phone’s address book—no IBAN needed. This matches Wero’s promise: “Just a phone number” for sending.

Important: A transfer cannot take place if the recipient doesn’t have Wero at their bank or hasn’t activated it yet.

- Entering the Amount and Message

We entered a small test amount (€0.01). The UI asked for the amount and, optionally, a message. After that, we tapped “Continue” and “Confirm.”

- Confirmation Step

A confirmation screen appeared, showing the recipient’s name, phone number, and amount. The bank clearly stated it’s an instant payment and free of charge. A final confirmation for security and it’s done.

The complete flow:

- Choose the Wero option

- Select a name from the address book

- Type amount

- Confirm

- Final confirmation

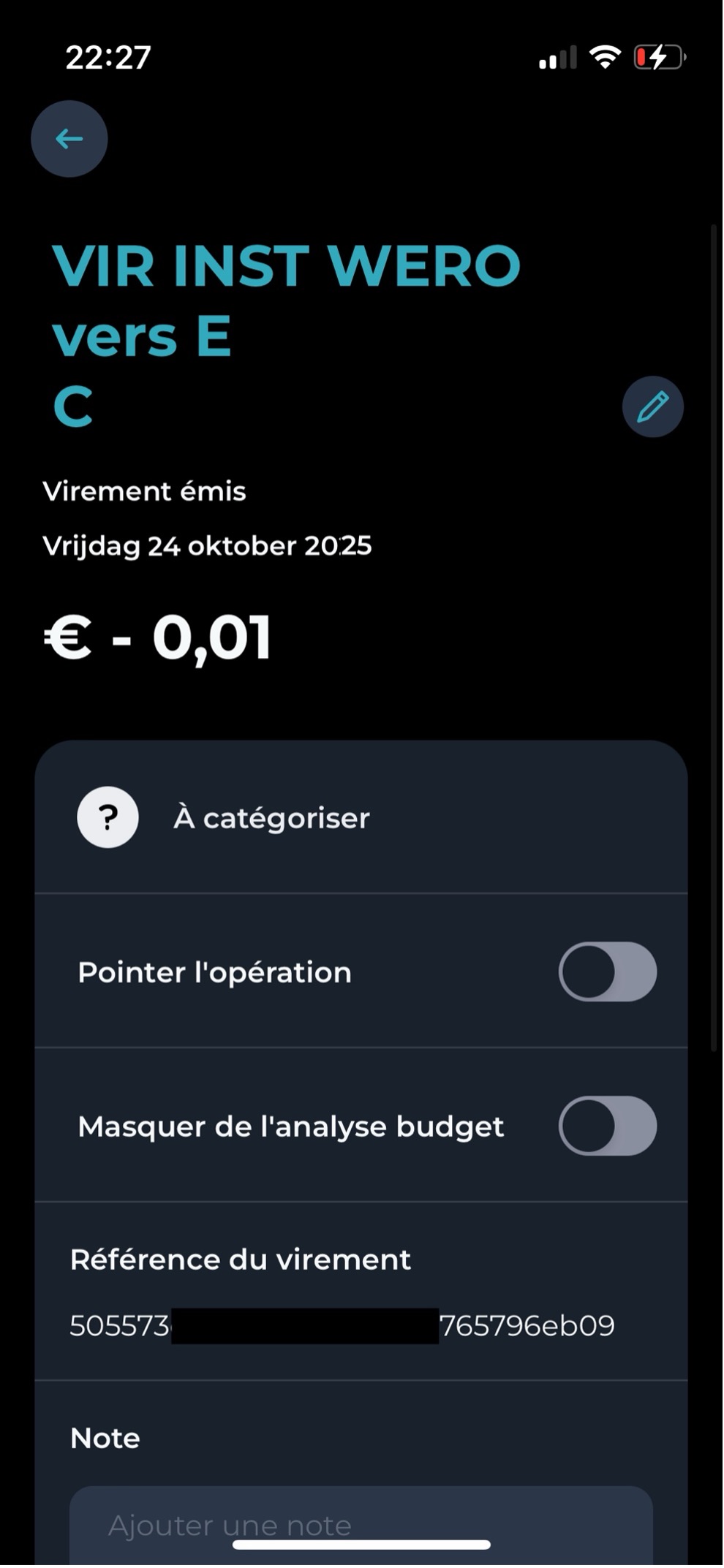

- Post-Transaction Overview

In our bank-app ledger, the entry shows: “VIR INST WERO vers…” with date, time, amount, contact name, and transaction reference. The flow is fully embedded and integrated as a normal instant payment in our bank app.

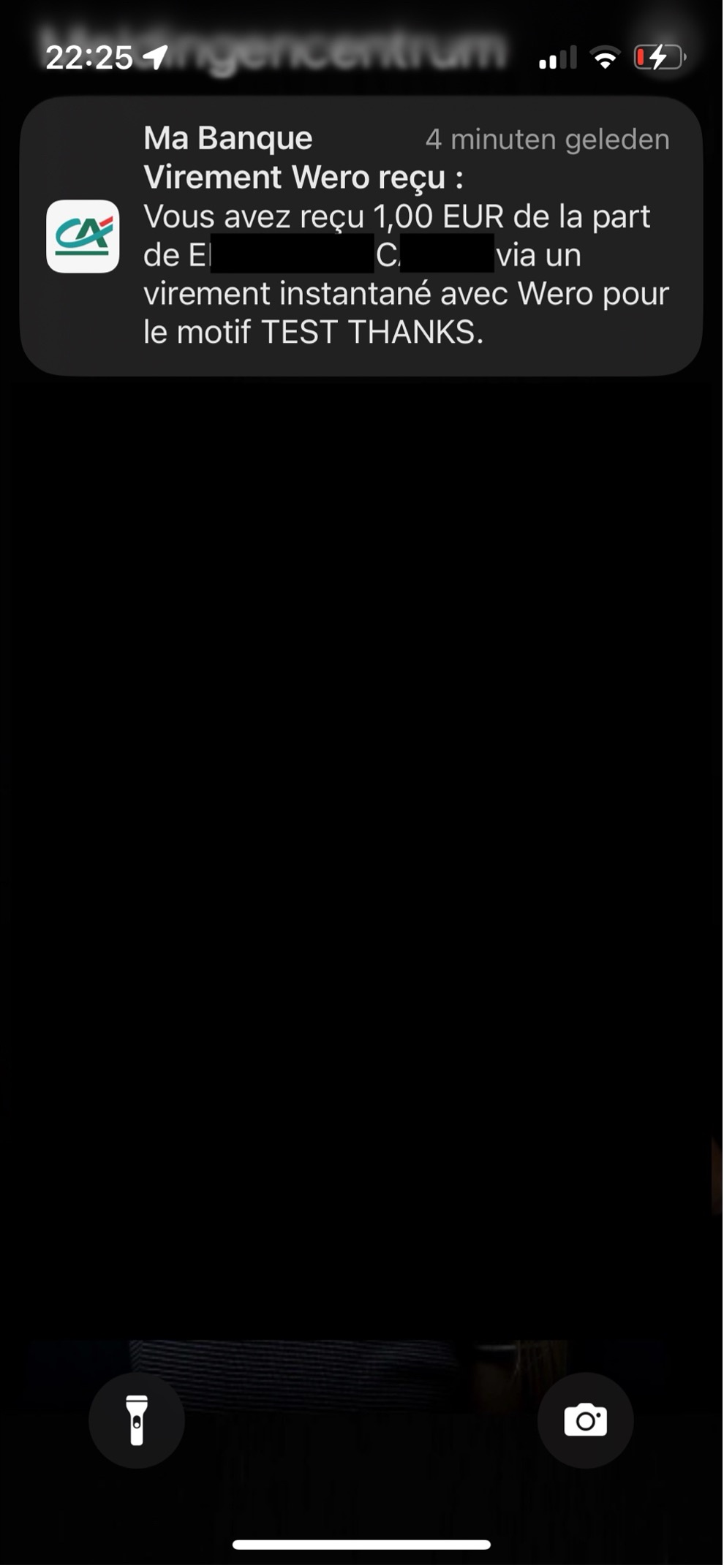

- Receiving a Transaction

Receiving is equally simple. Bank notifications showed us immediately that we’d received a Wero transaction. From Wero’s documentation: transfers happen in under 10 seconds. Our ledger immediately showed the received transaction with all details.

- Implicit Trust and Minimal Friction

No IBAN needed, no separate app to download. The sender enters a phone number and amount, the receiver gets money instantly. The entire process is intuitive.

Why This Matters for Payments Experts

✅ Embedded Bank-App Experience

Wero is embedded in the bank app. The bank remains central—not a third-party wallet, increasing user friction.

✅ Instant Account-to-Account via Phone Number

Sending via phone number (instead of IBAN) is a major convenience win. This signals that IBAN-first flows are under pressure. Simpler identification methods are preferred.

✅ Speed = Expectation

Instant settlement raises user expectations. With Instant Payments regulations active in Europe, consumers will expect immediate settlement as standard.

✅ Platform for Value-Added Services

Although Wero is currently P2P, the roadmap includes merchant payments, subscriptions, and more. Banks and PSPs must think beyond pure value transfer to ecosystem services: e-commerce checkout, loyalty, BNPL, etc.

✅ European Sovereignty

Wero is backed by European banks and rails, carrying a message of “More European control”. The question is whether this can be a real differentiator for merchants and PSPs operating in Europe.

⚠️ Things to Watch

- Network effect: Both parties must be on supported banks and geographies. The network is still building.

- Limited use-cases: Currently P2P focused. E-commerce launching soon, POS and cross-border still developing.

- Bank-to-bank variance: User education and UI may vary by institution.

- Fraud and risk: Identity and account linkage risks remain; banks must build appropriate controls.

- Monetization: If payment flows are low or zero-fee, value must be captured via adjacent services.

Strategic Recommendations

- Audit readiness: Assess account linking capabilities, UI/UX flows, instant settlement rails, fraud/risk controls, and reconciliation systems.

- User journey mapping: Compare phone-number flows versus traditional IBAN journeys. Identify where friction drops and data capture changes.

- Service-layer design: Consider add-ons like “split the bill,” payment request reminders, micro-payments, and cross-border transfers.

- Roadmap alignment: Treat Wero as a platform entry point for merchant checkout, subscriptions, loyalty, and BNPL.

- Competitive differentiation: Incorporate “instant phone-number pay” as a UX advantage. For banks: communicate European standard support to build trust.

- Data and analytics: Gather insights on contacts, usage frequency, and peer networks for segmentation and product design.

- Cost and pricing review: With instant account-to-account via SEPA Instant, pricing pressure is high. Adjust business models accordingly.

What This Means for Payments

This hands-on experience with Wero demonstrated that the vision is alive: instant, phone-number-based transfers embedded in a bank environment with minimal friction and high speed.

For payments professionals, this is a “proof point” of how modern P2P flows should look—and a signal of where we’re heading: a world where the bank app is the digital interaction hub, the phone number becomes the address, and value-added services ride on top of the rails.

Want to learn about what we can do to make your payment flow seamless? Contact us today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}